2016 Year End Recap & 2017 Outlook

2016 Year End Recap & 2017 Outlook

January 10th, 2017

Characterized by unexpected results and wild swings in financial markets and the political landscape, 2016 gave us one wild and crazy ride. If anyone predicted double digit returns in US equities, Great Britain exiting the European Union and a Trump victory in the US presidential elections, we would like a glimpse into their crystal ball for 2017.

In 2016 investors began the year focused on uneven economic data, anticipation of the Fed tightening monetary policy, stagnate corporate earnings, a precipitate drop in energy prices, a strengthening dollar and concerns surrounding China. These negative undertones led to the worst start to a year on record in regards to equity returns, with the S&P 500 delivering a negative 5.48% return in just the first two months of the year. As markets stabilized heading into the summer, the shock of Brexit threw the markets into a two day tailspin that resulted in a further drop in bond yields to new all-time lows and dragged equities down nearly 10% before stabilizing and returning to new all-time highs within two weeks.

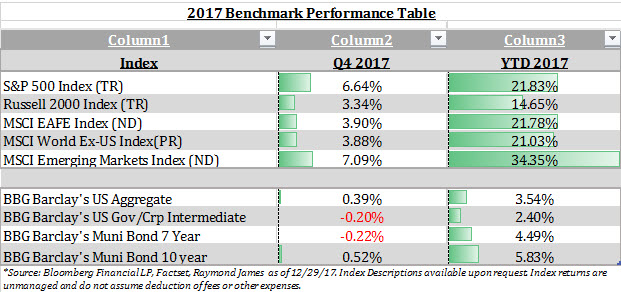

As the reality and uncertainty of Brexit sunk in, concerns over the state of the US economy abated and all eyes turned to the coming US presidential election. Considered a long shot in the early stages of the primaries, Donald Trump went on to shock the world in defeating Hillary Clinton. Most pundits (author included) warned that such a result would likely lead to a swift and substantial correction in risk asset prices, which most envisioned to be similar to the “Brexit correction”. Those predictions were not entirely incorrect, as we did see a very severe sell off in equities…that lasted mere hours. By the time markets reopened on November 9th, equity prices had stabilized and bond yields had moved up. This trend would persist through the remainder of the year eventually resulting in very strong fourth quarter returns in US equities and negative returns in bonds as yields continued to move up. At the end of the roller coaster ride, 2016 delivered very good returns in US equities, generally negative returns in developed international equities and generally flat returns in fixed income markets.

Through the course of the year we witnessed a shift in trends and sentiment that ultimately led to the results outlined above. Economically, investor’s confidence in the relative strength and trajectory of the US economy improved as the year progressed. Additionally, after nearly two years of stagnate or disappointing earnings growth, we began to see progress on this front in the second half of the year. While still subject to the shock of issues such as Brexit, US equity markets responded accordingly, grinding higher through the first three quarters of the year. Perhaps most importantly, we began to see optimism return to landscape for the first time in years, culminating with the 5+% post-election rally; where we witnessed the S&P 500 more than double its return from the first 10 months of the year.

Why optimism now? Currently markets are reacting not only to a higher degree of confidence in the economy and stronger earnings, but also to a president-elect whose campaign was long on promises. Trump’s campaign rhetoric included a number of potential policies seen as pro-business and pro-markets. Promises of tax reform (both corporate and business), regulatory reform (financial and healthcare related), fiscal stimulus (infrastructure spending) and incentives for companies to repatriate overseas profits all have the potential for stimulating higher growth (and inflation) and ultimately higher risk asset prices.

Trump also espoused a much more protectionist approach to global trade, which if pursued and enacted in the aggressive manner he outlined in his campaign, could prove to be a significant challenge for the US economy. There is also the question of coupling fiscal stimulus and lower taxes. The Republican Congress is likely to be hesitant to increase the budget deficit and add to our mounting national debt. It is difficult to recall a period in which policy has the potential for such a divergent set of outcomes and effects on the economy. Markets have clearly latched on to “the good” and are currently looking past the potential “bad”.

However, the market’s reaction in anticipation of said policies leaves us with some concerns. First, valuations are at or near all-time highs by many traditional measures. While valuation in and of itself is rarely, if ever a catalyst for a change in momentum, it will likely continue to be the biggest headwind for the markets. Also, we still don’t know what specific policy details the Trump administration will intends to pursue relative to the campaign rhetoric. It is unlikely that the ultimate result of any policy reform will be as hard lined as what we heard during the campaign, or even post-election. Finally, it takes time for policy change not only to be enacted (we are still dealing with Washington after all), but also to be felt in the economy. For example, cutting taxes tomorrow isn’t going to change trends in consumer behavior overnight, and any potential reforms to our national healthcare system likely wouldn’t go into effect until 2018 at the earliest.

So, how do we position for the coming year?

On the balance, we feel the good outweighs the bad in the current environment. Our view that the US economy is on firm footing, and we are seeing a shift in the underlying dynamics of the current cycle on several fronts. The recovery to date has been driven by easy monetary policy (low interest rates and quantitative easing) and surrounded by pessimism on the part of businesses, consumers and investors. We believe we will see a shift to a stage driven by optimism surrounding fiscal policy, tax reform and regulatory reform as well as a reboot to the earnings cycle. However, the apparent euphoria with which we ended the year is likely to subside in the near term, and we expect volatility to return to the markets as investors digest the extent and timing of the issues outlined above.

We expect to see a shift within US equities from more defensive positioning to more cyclical positioning. US smaller capitalization companies are likely to outperform their large cap counterparts. Small and mid-capitalization companies generate a higher percentage of their revenue from domestic operations, giving them less exposure to the negative effects of the strong dollar and greater leverage to improving US economic growth. These companies also carry a higher median tax rate, resulting in a greater benefit to corporate tax reform than large capitalization companies. Cyclical sectors such as financials and energy should be well positioned in 2017. The steeper yield curve (higher interest rates) benefits financial firms, while the rebound in energy prices continues to gain traction. High yield equity strategies are likely to underperform in the face of rising rates, as investors starved for income will have more options in the fixed income markets.

Developed International Markets remain undervalued, and we continue to believe that the improving fundamental back drop will lead to improved financial asset returns. Europe displayed positive economic trends in 2016 as the European Central Bank remained (and is likely to remain) extremely accommodative. Unemployment hit multi-year lows while manufacturing data hit multi-year highs. Great Britain will likely struggle through the realities of the Brexit process and could be an overhang on the region as whole. However, the disconnect between the economic and political environment could lead to a surprise to the upside. Meanwhile, Japan has made progress in structural reforms and corporate performance while domestic demand and monetary policy pushed GDP from .7% to 1.4% growth in 2016. The weak yen should continue to benefit earnings and we expect to see positive returns on a local currency basis.

Given the increase in inflation expectations and anticipated tighter monetary policy from the Fed, we expect to see a gradual rise in yields over the course of 2017. Post-election, we witnessed a swift and dramatic increase in yields across the curve from about 1.7% to about 2.5% on the ten year treasury (while municipal bond yields rose more on a relative basis). This dynamic carries both positive and negative implications. For income investors, the prospect of reinvesting future cash flows at higher rates is appealing. However, as rates continue to increase, bonds currently held in portfolios will reprice lower to reflect the change in yields. This will put pressure on total return in the near term.

Clearly 2017, as with most years, hinges upon the outcome of scenarios which are impossible to predict. This year, the overwhelming influence will come from the political landscape surrounding hot button issues such as tax reform, regulatory reform, repatriation and fiscal policy. We will be monitoring these factors extremely closely and communicating developments that may be pertinent to our positioning and strategy. 2017 could very well prove to be another rollercoaster ride, as the shifting dynamics we have outlined here are unlikely to take place without disruption and hic-ups.

We have begun our year-end review process and will be discussing any portfolio positioning, strategy or planning adjustments on an individual basis. As always, please do not hesitate to reach out directly to discuss any of the above information or implications to your personal strategy. We wish you a happy new year and look forward to serving you in 2017.

Best,

Josh L. Galatzan, CIMA®

Meridian Wealth Advisors

Managing Director & Founder

The content of this publication should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors on the date of publication and are subject to change. Information presented should not be construed as personalized investment advice or as an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned. Content is derived from sources deemed to be reliable.